by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

The number of new businesses has been on the decline since 2008, with more businesses closing than opening. The US Census Bureau confirmed the statistics, which was reported on by Gallup earlier this year. This startling trend also reaffirms a study released last year by the Brookings Institute, which noted that 2009, 2010, and 2011 saw the collapse of businesses faster than their creation.

The annoying thing about the Brookings Institute’s study is that they do not attribute the decline to anything in particular, saying that they need “a more complete knowledge about what drives dynamism, and especially entrepreneurship, than currently exists.” This is utter nonsense, and reinforces why I typically don’t pay attention to what the Brookings Institute says. They are providing political cover for the Obama Administration with their non-conclusive conclusion about the decline of new business.

The most suffocating factor is the sharp rise of federal regulations, which now cost the American economy nearly $1.9 trillion every year — more than 10% of our nation’s GDP. Add in state and local regulations, and that total is even higher.

Not surprisingly, the rates of business start-ups and deaths have changed for the worse as regulatory costs have grown. No wonder: Anyone who wants to stay in business has to keep finding more money to pay for higher costs, while anyone who wants to start a new business has to clear financial and legal barriers that get taller every year. The founder of Subway recently remarked that his company “would not exist” if today’s regulatory burden had existed when he started it in the 1960s.

Simply look at the past few years to see how the regulatory state has grown. Between 2009 and 2013, the federal government added $494 billion in regulatory costs to the American economy. The highlight was 2012, when President Obama and his executive agencies published over $236 billion in new costs. As for 2014, the federal government announced over 79,000 pages of new regulations, costing a total of $181.5 billion.

That’s equivalent to 3.5 million median family incomes. But it isn’t flowing to families through new jobs and higher wages — it’s lost on lawyers, paperwork and other compliance costs.

I was curious what some of the largest wealth managers had to say about the economy. Was anyone talking about the recovery (or lack thereof)? High taxes? Regulation? I took a sampling of the CEOs of Citigroup, JP Morgan Chase, Goldman Sachs, and Morgan Stanley to see what, if anything, they’ve publicly discussed in the last 6 months to a year. The only one that has spoken on the subject is Jamie Dimon of Chase, who stated earlier this year that “the U.S. economy is doing well” but he blamed poor government and regulatory policies for hurting growth. “We’re growing at 2.5 percent. We should be doing better. “I blame them all,” Dimon said of politicians. “To me, they waste a lot of time pointing fingers and not collaborating.”

But they do spend time regulating. This is the canary in the coalmine which impacts new and potential entrepreneurs. Many see the start up costs and the regulatory headaches as too burdensome a barrier to even begin, thus deciding it’s not worth it. Small businesses have been the backbone of America, the pathway to our greatness, and this recent, rapid decline in American business is most alarming.

by | ARTICLES, BLOG, ECONOMY, ELECTIONS, FREEDOM, GOVERNMENT, OBAMA, POLITICS, RETIREMENT, SOCIAL SECURITY, TAXES

I recently read a letter to the editor about Social Security in the Wall Street Journal that irritated me. Not the letter writer per se, but more by the Wall Street Journal choosing to print a letter that perpetuates a widely perceived myth about Social Security.

The letter was simply this: “Oh, please don’t blame older Americans for “eating up the budget” through payments of Social Security and Medicare benefits. It is the federal government that raided the Social Security Trust Fund. Older Americans have contributed to this for years. Where is the money now?”

The problem with this letter writer is that they really just don’t understand the truth that people who have paid into Social Security are getting many, many more times the actuarial value than what they put into it. It’s not a simple misunderstanding on this. It really, truly is just a flat-out lie that people who put 30-40 years worth of payments are merely getting back just what they put in.

The politicians need this lie to survive because they risk alienating a large voting bloc of older Americans if they merely even suggest that Social Security needs reform. But it does; the egregious state that Social Security is hidden by the way the federal government accounts for it. They even have a special name for it. Social Security is repeatedly described as a pay-as-you-go (“PAYGO”) system, which gives credence to something that is terribly incorrect. PAYGO is not a system at all; rather it is a method of reporting that hides earned realities, making it totally unacceptable to accounting professions, the SEC, and virtually everybody outside the government.

Calling it PAYGO helps to perpetuate the fallacy that beneficiaries are merely receiving what they paid into to. I don’t want to pick on the poor letter writer, as she doesn’t seem to really know how Social Security works (or hasn’t worked). But the Wall Street Journal should know better.

I suppose it is fitting that the 1936 Bulletin announcing Social Security ends like this: “What you get from the Government plan will always be more than you have paid in taxes and usually more than you can get for yourself by putting away the same amount of money each week in some other way.”

This is why we have accrued trillions in unfunded liabilities such as Social Security. If it sounds too good to be true, it probably is.

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

In lieu of the recent news that the GDP actually contracted during the 1st Quarter, some folks at the White House seem fit to blame both the winter and the actual process and algorithms by which 1st Quarter numbers are analyzed.

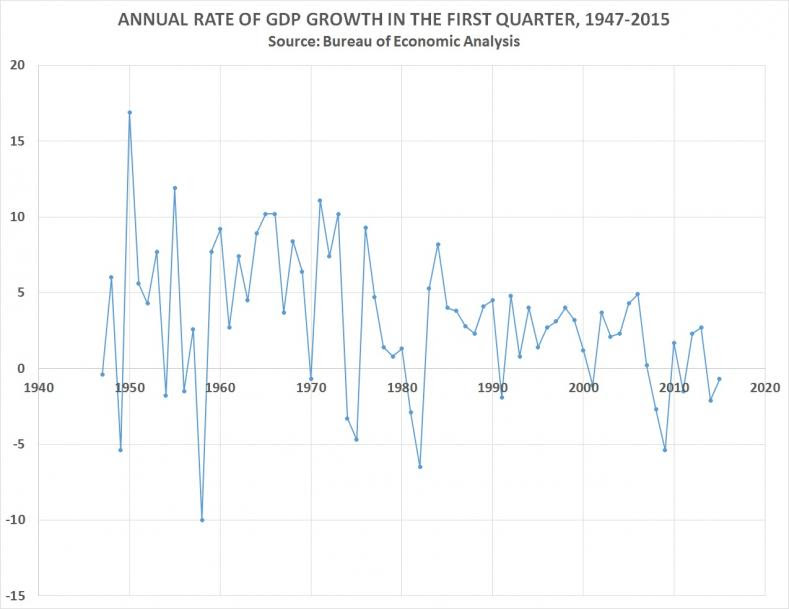

CNS News decided to take a look at Obama’s 1st Quarter numbers and compare them to previous presidents all the way back to 1947, which is the earliest data offered by the Bureau of Economic Analysis. The result shows that Obama has the lowest 1st Quarter numbers of all Presidents. I reproduced the article below, because it had some great graphs which shows the comparison data nicely. This just reaffirms what we know and what I wrote about the other day: the economy is still not that strong.

——–

Even if you leave out the first quarter of 2009—when the recession that started in December 2007 was still ongoing–President Barack Obama has presided over the lowest average first-quarter GDP growth of any president who has served since 1947, which is the earliest year for which the Bureau of Economic Analysis has calculated quarterly GDP growth.

In all first quarters since 1947, the real annual rate of growth of GDP has averaged 4.0 percent.

In the seven first quarters during Obama’s presidency, it has declined by an average of -0.43 percent. And if you leave out the first quarter of 2009 and look only at the first quarters of the six years since the recession ended, it has averaged only 0.4 percent.

In the six years of Harry Truman’s presidency for which the BEA has calculated quarterly GDP, the annual rate of growth in GDP in the first quarter averaged 4.5 percent.

During President Eisenhower’s eight years, it averaged 3.2 percent. During Kennedy’s three years, it averaged 4.9 percent. During Johnson’s five years, it averaged 8.3 percent. During Nixon’s six years, it averaged 5.3 percent. During Ford’s two years, it averaged 2.3 percent. During Carter’s four years, it average 2.4 percent. During Reagan’s eight years, it average 2.1 percent. During George H.W. Bush’s four years, it average 2.9 percent. During Clinton’s eight years, it averaged 2.6 percent. And during George W. Bush’s eight years, it averaged 1.7 percent.

President Obama took office on Jan. 20, 2009. In the first quarter of 2009, GDP declined at an annual rate of -5.4 percent. In the first quarter of 2010, it grew by 1.7 percent. In the first quarter of 2011, it declined -1.5 percent. In the first quarter of 2012, it grew 2.3 percent. In the first quarter of 2013, it grew 2.7 percent. In the first quarter of 2014, it declined -2.1 percent. And in the first quarter of 2015, it declined -0.7 percent.

In these seven first quarters that Obama has been president (2009 through 2015), the annual rate of growth in GDP has declined at an average rate of -0.43 percent.

But the National Bureau of Economic Research says the last recession, which began on December 2007 did not end until June 2009. If you leave out the first quarter of 2009, and only count the six years (2010-2015) since the recession ended in June 2009, real annual rate of growth of GDP in the post-recession first quarters of Obama’s presidency has averaged 0.4 percent.

When GDP declined at -1.5 percent in the first quarter of 2011—which was after the recession and two full years into Obama’s presidency—some blamed it at least partly on the weather.

“Some of the slowdown in growth was linked to bad weather in early 2011 and an 11.7 percent decline in defense spending,” said a Reuters story of May 27, 2011.

When real GDP declined at a rate of -2.1 percent in the first quarter of 2014, a May 30, 2014 New York Times story said: “Most economists on Wall Street and at the Federal Reserve blame a very cold winter for much of the slowdown.”

When real GDP declined at a rate of -0.7 percent in the first quarter of this year, the top paragraph of an Associated Press story said: “The U.S. economy shrank at a 0.7 percent annual rate in the first three months of the year, depressed by a severe winter and a widening trade deficit.”

But there seems something more at work here than climate patterns–or the Obama presidency.

Under previous presidents, real GDP sometimes grew massively during the first quarter. In 1950, under Truman, for example, GDP grew at an annual rate of 16.9 percent in the first quarter. In 1955, under Eisenhower, it grew at a rate of 11.9 percent.

Under Johnson, in the first quarters of both 1965 and 1966, it grew at a rate of 10.2 percent. Under Nixon, it grew at 11.1 percent in the first quarter of 1971, and 10.2 percent in the first quarter of 1973, it grew at 10.2 percent.

Under Ford, in the first quarter of 1976, it grew at 9.3 percent. Under Reagan, in the first quarter of 1984, real GDP grew at a rate of 8.2 percent.

But since 1984—more than three decades ago–there has been no first quarter, in any year, under any president, when real GDP grew even as fast as 5.0 percent. The closest it came was in the first quarter of 2006, when George W. Bush was president, and it hit 4.9 percent.

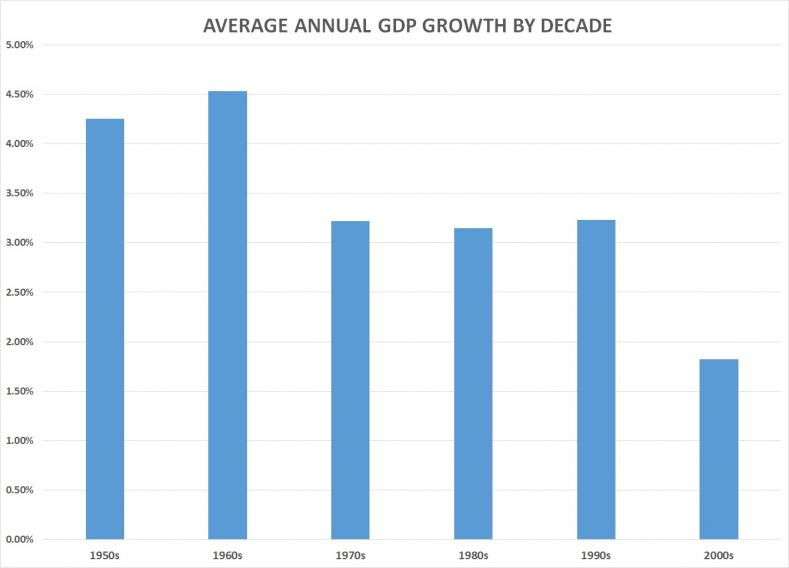

In the decades starting after World War II, average annual growth in GDP peaked in the 1960s.

In the 1950s, annual growth in GDP averaged 4.25 percent. In the 1960s, it climbed to 4.5 percent. But it dropped to 3.22 percent in the 1970s, then 3.15 percent in the 1980s, before ticking up to 3.23 percent in 1990s. In the 2000s, it averaged only 1.82 percent.

In the first five years of this decade (2010-2014), annual growth in GDP has averaged 2.2 percent. But that is less than the 2.7 percent it averaged in the first five years of the last decade (2000-2004) which was before the recession hit at the end of 2007 and brought the decade’s average down to 1.82 percent.

If it were to maintain an average annual rate of 2.2 percent for the next five years, the American economy of this decade would still be growing at less than half the rate of the 1960s.

Should the long-term decline in U.S. economic growth be attributed to cold weather? Or should people in Washington, D.C., start looking around them for an anthropogenic cause.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, OBAMA, POLITICS, TAXES

I came across this little piece in the NYPost discussing the sluggish economy and the arbitrary numbers that come out of the Labor Department. It starts off discussing the 1st Quarter GDP contraction, which stumped many “economists”, and even went so far as to possibly blame the algorithms themselves by which the government analyzes 1st Quarter numbers. Because it certainly couldn’t be domestic policies, could it?

This writer posits that we could indeed be on the bring of a recession, the definition of which is 2 straight quarters of economic contraction, and points out something fairly obvious. People just don’t have a lot of money to spend. I concur this is a major part of assessing the health of an economy, although I would argue that investment spending spurs economic growth even more than consumptive spending, which is this writers argument. Putting that aside, however, he does a decent job pointing out the concerns about the economy that we should all be paying attention to. Here’s the article and food for thought below:

“Anyone with even a quarter of a brain now understands that the US economy got off to a bad start this year.

There was an economic contraction in the first three months — when the nation’s gross domestic product fell at an annualized rate of 0.7 percent — that some quarter-brainers are still blaming on the cold weather, strikes at ports, the strong dollar, solar flares, Martian landings and (insert your own poor excuse here).

The truth: Most of these excuses are part of the problem, although I didn’t personally see or not see the Martians.

But the biggest part is that people don’t have enough money to spend. Interest from savings is down to zero, people don’t liquidate stock gains to make purchases, and job and income growth has been sketchy.

The economy isn’t doing much better in the current quarter either. The Federal Reserve Bank of Atlanta, an independent observer if ever there was one, measures growth so far in the second quarter at an annual rate of just 1.1 percent. That means growth — un-annualized — is a paltry 0.275 percent with less than four weeks left in the quarter.

It’s quite possible that we will eventually be told, after all revisions are made, that the economy met the official definition of a recession in the first half of 2015, which is two straight quarters of contractions.

But the quarter-brainers will probably get something to cheer about when Friday’s employment numbers come out. And, if they don’t strain their quarter-brains looking too deeply into the numbers, they could come away with a smile that can only happen because ignorance is bliss.

Wall Street expects the Labor Department to report that 235,000 new jobs were created in May. That would be higher than the 223,000 new jobs that — before any revisions are made — were created in April.

I’ve written before about the so-called birth/death model, which is the government’s fist-on-the-scale way of adding jobs they assume but can’t prove exist when new companies suddenly come into business in springtime.

The only problem is, entrepreneurs — especially those just starting out and risking their own capital — aren’t very daring when it’s clear to everyone that the economy isn’t doing well. So maybe, just maybe, there are more companies dying this spring than being born.

Labor must be having some second thoughts about the validity of that model since it guessed that only 213,000 phantom jobs were created by newly born companies in April. That’s way down from the 263,000-phantom-job guesstimate in April 2014.

The guesstimate for May should still be substantial. In May of 2014, Labor’s phantom jobs guesstimate added 204,000 jobs. Even if that’s been adjusted downward, this will still give a nice boost to the job growth that will be reported Friday.

There’s no guarantee, of course, that Friday’s number will be good. Any number of things could go wrong. Seasonal adjustments could hurt Friday’s number. And, of course, companies could have actually cut jobs in April. There were plenty of announcements of such cuts.

So, will Wall Street get the 235,000-job growth it expects? I say there’s a 60 percent chance Friday’s number meets or exceeds that guess.

But even if you guess right on Friday’s jobs figure, the prize could be elusive. Most folks don’t know how Wall Street will react to a better-than-expected number. If the figure is too strong, it’ll causes interest rates to rise and bond prices to fall in anticipation that the Federal Reserve’s interest rate hike is back on the table. If the number is weaker than expected, even the quarter-brainers will start worrying the economy is tanking.”

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

As Chris Christie is still contemplating a 2016 presidential run, he recently posited a tax reform plan that differentiated himself from many of the other possible contenders. His platform was comprised of several points, such as: lower tax margins, reforming regulation,and eliminating payroll taxes for some earners. The last major tax code overhaul was the 1986 IRC reforms under President Reagan.

With regard to lowering tax margins, Christie proposed a true tax cut for both individual and corporate rates. Christie’s pan brings the top marginal rate to 28% from its current 39.6% for highest earners. His bottom rate would be less than 10% with just one more rate in the middle. Christie also proposes lowering the corporate tax rate from 35% to 25%. Currently, we have the highest corporate tax rate in the world. This would give businesses a much-needed boost.

Another part of this plan goes after regulation. Christie nails it when he stated, “Regulation must be rational, cost-based and used only to implement actions that are explicitly authorized by statute. This era in which an ideological administration tries to accomplish through the regulatory state what it didn’t have the votes to accomplish in the duly elected Congress must end.” The brutal, overbearing regulatory environment that currently exists is often overlooked, and I applaud Christie for bringing attention to it.

Christie also examines the payroll tax, calling for its elimination for those over 62 and under 21, which would “reduce the marginal cost to the employee of taking a job, and reduce the federally imposed cost to an employer of hiring someone.” It is an incentive for older workers to continue working and younger workers to start. With the workforce participation rates at all-time lows, this is a pro-growth approach.

Other tenets of his plan include increasing investment in R&D and developing a more sensible national energy plan, such as building the Keystone pipeline. It is revenue-neutral, meaning the tax cut side will be offset by modifying or eliminating many of the tax credits and deductions that riddle the tax code, making it much more simplified. Keenly aware of the cherished mortgage deduction and charitable contribution deduction, Christie makes those basically off-limits, but the rest of them could be fair game.

Christie has yet to decide and announce if he is actually running, but his ideas provide good fodder for, and comparison to, the other current candidates. Some have called for a Flat Tax, while others champion a national sales tax. Tax code reform is overdue and necessary, and should be a centerpiece of any serious candidate for 2016. Overall, Christie’s plan is fairly sensible and growth-oriented. Now if he would only fix his entitlement reform policies!

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

Recently, a business owner in the heart of Baltimore penned a piece describing some of the excessive and burdensome government policies business owner face. His piece gave an eye-opening view of the reality that is decades of fiscal and governmental mismanagement in the city.

For instance, he notes there a fee or fine for a ridiculous amount of infractions: “When the building alarm goes off, the police charge us a fee. If the graffiti isn’t removed in a certain amount of time, we are fined. This penalize-first approach is of a piece with Baltimore’s legendary tax and regulatory burden.”

As for taxes, “Baltimore fares even worse than other Maryland jurisdictions, having the highest individual income and property taxes at 3.2% and $2.25 for every $100 of assessed property value, respectively. New businesses organized as partnerships or limited-liability corporations are subject, unusually, to the local individual income tax, reducing startup activity.” This policy is especially anti-business; a company’s early make-or-break years are impeded by an excessive tax burden.

And regulations? “State and city regulations overlap in a number of areas, most notably employment and hiring practices, where litigious employees can game the system and easily find an attorney to represent them in court. Building-permit requirements, sales-tax collection procedures for our multistate clients, workers’ compensation and unemployment trust-fund hearings add to the expensive distractions that impede hiring.” People go into business to make things, to provide a product, a service, not to comply with government red tape.

So what is the solution? Typically more money is the stock answer from the Democrats but in the case of Baltimore, even that’s not true. They’ve already tried that. “The Maryland state and Baltimore city governments are leveraging funds to float a $1 billion bond issue to rebuild crumbling public schools. This is on top of the $1.2 billion in annual state aid Baltimore received in 2015, more than any other jurisdiction and eclipsing more populous suburban counties. The financial problem Baltimore does face is a declining tax base, the most pronounced in the state. According to the Internal Revenue Service, $125 million in taxable annual income in Baltimore vanished between 2009 and 2010.”

A declining tax base can be reversed once the climate for business growth and opportunity changes. Instead of approaching businesses merely as a source of revenue for a fiscally mismanaged city, give them breathing room. Loosen the regulations. Repeal fees and fines. Lower the tax burden. Give them the tools necessary to grow their companies and create more jobs.

Baltimore has suffocated under the failed progressive policies of the last few decades — the city and the state and local government all run by Democrats. What they’ve done is bad, but what they haven’t done for businesses is even worse.

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

I’ve written several times over the years about Obama’s economic policies and anti-business climate as factors that have hampered this country’s growth and recovery. Phil Gramm has a good piece in the WSJ recently that gave a succinct overview of all that is still wrong with the economy. Obama continues to insist that either a) the economy is good or b) any problems are someone else’s fault. Do yourself a favor and read this piece which is sobering, but accurate, about the state of our economy today.

What’s Wrong With the Golden Goose?

Since the Obama recovery began in the second quarter of 2009, public and private projections of economic growth have consistently overestimated actual performance. Six years later, projections of prosperity being just around the corner have given way to a debate over whether the U.S. has fallen into “secular stagnation,” a fancy phrase for the chronic low growth seen in much of Europe.

This is just another in a long line of excuses. America’s historic ability to outperform Europe is well documented; we call it American exceptionalism. It has always been based on the fact that the U.S has had better, more market-driven economic policies and our economy therefore worked better. But, as the U.S. economy is Europeanized through higher taxes and greater regulatory burdens, American exceptionalism is fading away, taking economic growth with it.

How bad is the Obama recovery? Compared with the average postwar recovery, the economy in the past six years has created 12.1 million fewer jobs and $6,175 less income on average for every man, woman and child in the country. Had this recovery been as strong as previous postwar recoveries, some 1.6 million more Americans would have been lifted out of poverty and middle-income families would have a stunning $11,629 more annual income. At the present rate of growth in per capita GDP, it will take another 31 years for this recovery to match the per capita income growth already achieved at this point in previous postwar recoveries.

When the recession ended, the Federal Reserve projected future real GDP growth would average between 3.8% and 5% in 2011-14. Based on America’s past economic resilience, these projections were well within the norm for a postwar recovery. Even though the economy never came close to those projections in 2011-13, the Fed continued to predict a strong recovery, projecting a 2014 growth rate in excess of 4%. Yet the economy underperformed for the sixth year in a row, growing at only 2.4%.

Implicit in these projections and in the headlines of most economic news stories—which to this day blame cold winters, wet springs, strikes, hiccups and blips for America’s failed recovery—is the belief that there has been no fundamental change in the U.S. economy. Underlying this belief is the assumption that either the economic policies of the Obama administration are not fundamentally different from the policies America has followed in the postwar period or that economic policy doesn’t really matter.

And yet we know that the Obama program represents the most dramatic change in U.S. economic policy in over three-quarters of a century. We also know from the experience of our individual states and the historic performance of other nations that policy choices have profound effects on economic outcomes.

The literature on economic development shows that U.S. states and nations tend to prosper when tax rates are low, regulatory burden is restrained by the rule of law, government debt is limited, labor markets are flexible and capital markets are dominated by private decision making. While many other factors are important, economists generally agree on these fundamental conditions.

As measured by virtually every economic policy known historically to promote growth, the structure of the U.S. economy is less conducive to growth today than it was when Mr. Obama became president in 2009.

Marginal tax rates on ordinary income are up 24%, a burden that falls directly on small businesses. Tax rates on capital gains and dividends are up 59%, and the estate-tax rate is up 14%. While tax reform has languished in the U.S., other nations have cut corporate tax rates. The U.S. now has the highest corporate rate in the world and the most punitive treatment of foreign earnings.

Meanwhile, federal debt held by the public has doubled, so a return of interest rates to their postwar norms, roughly 5% on a five-year Treasury note, will send the cost of servicing the debt up by $439 billion, almost doubling the current deficit.

Large banks, under aggressive interpretation of the 2010 Dodd-Frank financial law, are regulated as if they were public utilities. Federal bureaucrats are embedded in their executive offices like political officers in the old Soviet Union. Across the financial sector the rule of law is in tatters as tens of billions of dollars are extorted from large banks in legal settlements; insurance companies and money managers are subject to regulations set by international bodies; and the Consumer Financial Protection Bureau, formed in 2011, faces few checks, balances or restraints.

With ObamaCare the government now effectively controls the health-care market—one seventh of the economy. The administration’s anti-carbon policies hamstring the energy market, distort investment and lower efficiency. Despite the extraordinary bounty that has flowed to America from an unfettered Internet, Mr. Obama has dictated that the Web be regulated as a 1930s monopoly, bringing the cold dead hand of government down on what was once called the “new economy.”

During Mr. Obama’s presidency, the number of Americans receiving food stamps has risen by two-thirds and the number of people drawing disability insurance is up more than 20%. Not surprisingly, labor-force participation has plummeted. Crony capitalism and artificially low interest rates have distorted the capital markets, misallocating capital, overpricing assets and underpricing debt.

Despite the largest fiscal stimulus program in history and the most expansive monetary policy in more than 150 years, the U.S. economy is underperforming today because we have bad economic policies. America succeeded in the Reagan and post-Reagan era because of good economic policies. Economic policies have consequences.

With better economic policies America was like the fabled farmer with the goose that laid golden eggs. He kept the pond clean and full, he erected a nice coop, threw out corn for the goose and every day the goose laid a golden egg. Mr. Obama has drained the pond, burned down the coop and let the dogs loose to chase the goose around the barnyard. Now that the goose has stopped laying golden eggs, the administration’s apologists—arguing that we are now in “secular stagnation”—add insult to injury by suggesting that something is wrong with the goose.

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, RETIREMENT, SOCIAL SECURITY, TAXES

Chris Christie recently unveiled a plan to overhaul Social Security. This is his Hail Mary to get back in the game of running for President. Though I applaud his decision to make entitlement reform a major portion of his platform, his proposal is merely another veiled tax increase on the wealthy.

There are two portions to his reform plan. The first is to raise the retirement age from 67 to 69 over a phased in length of time. That is not such a bad idea. It is the second portion, related to reducing and even eliminating entirely the ability for a taxpayer to receive Social Security, into which he has paid during his working career, that is particularly heinous.

Chris Christie’s proposal to reduce and eliminate Social Security benefits for wealthier people is just a capitulation to the Left. He advocates reducing benefits for retired persons if they earn more than $80,000 and calls for eliminating outright Social Security benefits for retirees who earn $200,000 or more a year. This is basically another massive tax increase on the wealthy disguised as entitlement reform.

For many upper income earners, their income tax rates are already over 50%, especially when local and state taxes are factored in. Yet when one calculates that income tax rate, not included in that amount is Social Security (though Social Security is a separate tax). As reference, for those who are self-employed, one pays 15.3% to Social Security, but if someone is employed, the employer pays 7.65% while the employee pays the other 7.65%. The reason why this tax is not considered in the tax rate calculation is because it is considered to be “retirement pay”, something paid into “the system”, based upon the “promise” that it will be returned as benefits at a point in the future.

But now Christie proposes to change the game in a nearly fraudulent way. Social Security taxes would still be collected from taxpayers, but for upper income earners, you won’t get your benefits back in entirety or even at all after a certain income level when you are of retirement age. That’s practically criminal. It’s raising taxes on the wealthy yet again, because the Social Security tax would still be collected over the years, but you don’t receive the promised benefits anymore past certain income levels during your retirement years. Looked at it another way, if you are successful, if you do well and are able to retire with a decent income stream, you are now punished for that success and lose the funds you faithfully paid in over the years because the government now deems you to have too much money. It is wealth confiscation to cover decades of mismanaged funds that now need massive reform to be solvent.

I think Chris Christie’s heart is in the right place, but he really hasn’t thought his plan through. It plays directly to the Left playbook on class warfare, implying that the wealthy need to “pay their fair share” by now forfeiting their Social Security funds past a certain income threshold in order to help pay for government fiduciary malfeasance. That concept is repugnant and Social Security reform needs a better plan than what Chris Christie has to offer.

by | ARTICLES, ECONOMY, RETIREMENT

Everyone thinks they can retire at age 65. It’s an American ideal born in the last century with the rise of unions, the defined benefit plan, and generous pension systems. In reality, especially due to advances in health, medicine, and nutrition, many people have great capability to continue to work and contribute to society and themselves until 80. And they should — because they need to.

There is a crisis of affordability looming. Besides the enormously wealthy, for the most part no average person can afford to retire at 65. It is simply not possible, living a normal lifestyle, for anyone to put enough toward retirement that will enable him to live another 20-30 years. A life span of 85-95 is swiftly becoming the new norm. The only workers today who are the exception to this reality, and have any hope of a lengthy retirement with comfort, are public service employees.

Taxpayers have been long bamboozled into making generous commitments to the retirement systems of public service workers. All over the country, in all levels of federal and state governments, these defined benefit plan pension funds have proven to be vastly untenable. Yet to sustain the plans in their current arrangements and cover the obligations that have already been promised, the rest of society will be duty-bound/compelled to contribute to the retirement of those public service workers via higher taxes. This is turn makes the rest of the populace poorer — because their hard-earned money is being levied to the promised public pensioner, and not for able to be saved for themselves.

The grand scheme is becoming unhinged. One must realize that the more people continue to buy into the idea that they are supposed to “retire at 65”, the more they are suckered into continuing make their retirement years poorer and subsequently make the retirement years of public service employees richer. People see a public service worker being able to retire at that age and they think “I should be able to also do so”. This idea needs to change.

There are two reasons why most people think that such pension programs are still sustainable and normal: their troubles are largely masked because they encompass the larger budget process of federal/state/local governments (and how many people pay attention?) and the costs to keep the programs afloat are borne by all the rest of society — the taxpayers. This arrangement enables a small group of people to be paid a sizeable and continuous pension for until death. It is not out of the ordinary anymore for a person to receive $65K- $100K for the rest of their life. But the actuarial cost to provide that promised benefit is astronomical.

With the lifespan of Americans growing longer, retiring at 65 is no longer viable; the systems are badly strained. And it is certainly not rational for the longevity of Social Security and Medicare either. Yet the steadfast refusal of most of government to overhaul retirement systems or make age and formula adjustments to entitlement programs — in order to maintain this retirement facade — only compounds the problem.

Another one of the biggest detriments of being able to retire at 65 is investment return. Interest rates have been historically low for the last six years and there is a strong likelihood of them staying low for another few. As a result, peoples’ retirement portfolios have lagged in their anticipated growth and goals. The low rates mean less money overall for retirement time, a problem which can be offset by continuing to work and contribute to a retirement fund past the basic age.

Likewise, inflation is not the issue that everyone thinks it is. The true problem is the cost of living — but really, it’s the cost of modern living, the “keeping up with the Jones”. For example, newer models of everything due to technology constantly changing — upgrading TVs, cell phones, etc. are raising the bar for how much pensioners want to comfortably live on and live with.

In sum, with living longer, low rates of return, and the “cost of Jones’s increase”, people must begin to realize that the time span between 65 – 80 can be, and should be, a healthy and productive time of life. Working, staying active, and continuing to save will be beneficial in the long run. The mindset of older citizens needs to change and they need to understand that they can should aim to be productive until they are 80. At 65 they can certainly slow down, but the concept of retiring and not working anymore at that age is unrealistic and unaffordable.

UPDATE (5/5/15): USA Today has an article today just on this subject: “Traditional retirement possibly becoming a thing of the past”:

“A new survey of American workers from the Transamerica Center for Retirement Studies found that 82% of the respondents age 60 and older either are, or expect to keep working past the age of 65. Among all workers, regardless of age, 20% expect to keep on working as long as possible in their current job or a similar one.

“The days of the gold-watch retirement where we have an office party and maybe some punch and cookies and never work again are more mythical than a reality,” said Catherine Collinson, president of the retirement studies center. “Very few workers actually envision that type of retirement and many plan to keep on working part-time even after they retire.

“It even raises the question is retirement the right word.”

by | BLOG, ECONOMY, TAXES

People have traditionally measured wealth by the amount of tangible assets they have. Viewed from this perspective, many people who have saved substantially for their retirement through an IRA, a 401K, or other profit sharing plans, (all in the category known as defined contribution plans) are well up in the highest percentile of people with wealth. Other people have retirement plans that provide only income streams for their (and often their spouse’s) lives. These are known as defined benefit pension plans. But since they do not have a pool of assets in a separately owned account, having rights only to the income stream – they are not viewed as having actual assets.

Therefore, these people are very often at the low end of the “asset” wealth scale. But the income stream is certainly an asset, a quite valuable one. And because of government policy and other economic factors in the last few years, the value of the defined benefit plans has exploded compared to the value of defined contribution plans. This has created a massive wealth switch to public service employees from private sector employees.

Given what the federal government’s policy has been with interest rates and fiscal policy, and given the much lower rate of return we have had to endure these last 6 years, the value of the retirement income stream has grown enormously, while the value of the retirement “nest egg” has diminished correspondingly. In this way, there has been a real conversion of income and assets such that people with continual income streams from defined benefit plans can now be looked at as having substantial “assets” while the retirement portfolio earning very little interest is less desirable. Being considered “wealthy” has become more about with having financial security than assets. The main reason for this switch can be found by examining the state of the pension system.

Say you have two people — one person in private industry, and one in the public sector, both making say $70K/year and hoping and expecting that they could retire on, say, $50K per year for all their years of good service and hard work.

It used to be, up until about 6 years ago, that a private industry person retiring with that $50K/year plan in mind could actually retire on that. The sum of his portfolio that would enable him to retire with that much per year would be around $1 million .That person could reasonably have concluded that he is set pretty well for life; if his portfolio earns 5% a year, he could pull out that $50k a year (5-% on a $1 million ) and still have the principal ($1 million ) left to pass on to the kids.

In a similar way, a public service worker or union making the roughly the same money would have roughly similar expectations — a $50K yearly pension. You could put a value on it ($1 million) but there is a large difference between the public pension and private pension. When the public pensioner dies, that pension ends; the money is gone. That is, there is no principal because there is no personal “investment portfolio” in the same manner that a private sector pensioner has. The public pension is funded from the larger investment pool within the public service industry.

Now, the last six years has made the pension and investment situation for retirees quite untenable. Interest rates remain sluggish, yielding only around 2% a year. That becomes only about $20K in returns for the private industry person. Now the pensioner can’t live off of the returns from the million in his portfolio. It’s not going to give him the retirement he planned or the inheritance he thought he could pass on. He needs more.

The situation is different for the public service person. He still gets his $50k a year, regardless of whether the return is actually 2% or 5%. His defined benefit plan promised to pay him a set amount every year until he passes away. When these plans were funded, and interest rates were a reliable 5%, the public service employers were only putting away enough to have $1 million worth per person, counting on yearly investment returns of 5%.

In order for the public service pension to get funded as promised , (at $50K/yr) the public service pension pool must pay it. Though the plan may have been “worth” a $1 million, now that the pool has to cough up the difference in funds due to low investment performance (2% in reality when 5% was necessary). That pension now becomes the valued at $2.5 million, ($2.5million x 2% = $50,000) because more funds are needed to supplement it in order to maintain the promised payments.

The government must come up with that extra $1.5 million supplement to sustain the promised benefits to the public service person. Multiply that by for every person for which there is not enough money set aside in these pooled retirement funds to pay for them. Where does that money come from? The employer? No, the taxpayer.

Here’s the kicker. When the public sector and unions earmarked that million for the employee, they hoped it would be enough to cover it. Within the private sector, over time business owners began to understand the fiscal instability and risk inherent in such defined benefit plans. Refusing to make such a commitment, most private sector employers have abandoned such plans completely.

When the public service sector started seeing the fissures in the system, they started to negotiate to keep their benefits as good as possible. But they didn’t, and still don’t, negotiate with the taxpayer. They negotiate with politicians, not the people who fund the retirement pool.

So what has really happened with these public and private retirement plans? Those public service persons with the $50K retirement plan saw the value of their retirement jump from $1 million to $2.5 million. From an accounting point of view, it’s money going into the assets of the public service employees, while the other side is a debt born to all the taxpayers for the benefit of a few.

This is nothing more than a huge wealth transfer. When the public sector and unions made deals with municipalities, these were cozy sweetheart deals, a trojan horse, a poison pill. There were no provisions made to handle the possibility of a low-interest rate society; they took their chances and their fallback was to suck money from the taxpayer by raising taxes to cover budgeting shortfalls.

Now the private sector pensioners are bearing the brunt on two fronts — their own retirement plans are performing poorly and their portfolios are dwindling while their taxes help to fund the gross negligence of the public sector. All taxpayers are feeling the pinch. The failure of the public service groups to be responsible in their fiduciary responsibility to the taxpayer means that now more than ever, vast amounts of wealth are being given over merely to band-aid this broken system, mask the true debt, and avoid real reform. This is politician/public service union cronyism for all to see.