by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, QUICKLY NOTED, TAX TIPS, TAXES

Since there seems to be increased interest, and confusion, regarding tax filing and Obamacare this year, it is worth it add some more information to help navigate the process.

The IRS Tax Form 1095a is officially known as the “Health Insurance Marketplace Statement”. If a household member or members enrolled in a healthcare plan through a state or federal exchange, you will receive a 1095a in the mail by early February. You cannot file your taxes without it. It contains information regarding your coverage, such as the number of people enrolled in a marketplace plan, and the dates of effective coverage.

Please note: you will not receive a Form 1095a if you have health coverage through a job or through programs such as Medicaid, Medicare, or the Children’s Health Insurance Program (CHIP).

What you will see on a Form 1095a?

–The form will have information about every member of your household who received Obamacare coverage in 2014. Each person will be listed separately.

–The form will list month-by-month, the amount you paid for your health insurance premium. Each person will be listed separately.

–The form will provide the amount of the “premium tax credits” you received in 2014. They are also called “advanced payments”. This amount is what lowered your monthly premiums, and was calculated based upon income information you provided when you enrolled.

–The form will list the cost of a “benchmark” premium that your premium tax credit is based on. This was the second-lowest cost silver plan, and was considered the “benchmark” to determine subsidies for lower- and moderate-income earners who enrolled in Obamacare.

Why is the 1095a necessary?

The 1095a is your PROOF OF INSURANCE. It contains all the information you need to fill out your form 8965, which is the Premium Tax Credit form. The 8962 Form is a worksheet, whose calculation gets recorded on your 2014 Tax Return.

The main point of all of these forms is really the Premium Tax Credit portion. Remember, 85% of Obamacare enrollees received some sort of subsidy, which is properly known to the IRS as a “Premium Tax Credit”. But most people opted not to receive their tax credit at tax filing time (now). They received it in advance, during 2014, in the form of monthly amounts that were credited against the monthly healthcare premium costs. These advance payments lowered the monthly cost of insurance.

The credit was tabulated based on estimated income information furnished during the application process. But because income situations can change over the course of a year (remember you enrolled at the beginning of 2014), the IRS requires you to re-calculate your income again at tax time (now), and match it against the amount and information you provided when you enrolled.

Since your Premium Tax Credit was based upon estimated income amounts, the amount you were eligible to receive as a tax credit may be higher or lower than what you actually did receive. So, using the information you receive on your 1095a about your household and your payments and your subsidies, you then fill out the Form 8962 to calculate the ACTUAL amount of tax credit you were eligible for in 2014, and check it against what you received as an advance payment applied to your monthly premium costs. Any differences will be resolved either by either reducing or increasing your tax credit amount, which will then affect the final amount of taxes due or taxes returned to you.

Also note — if you enrolled in Obamacare, you must fill out Form 8925, which means you cannot file a 1040EZ. You must file a traditional 1040 tax return.

All the information listed above that you will see on the 1095a is important. If there are any errors, it is imperative that you contact the Obamacare marketplace immediately to resolve the inconsistencies before you file your taxes.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

Since we’ve been discussing it recently.

by | ARTICLES, BLOG, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAX TIPS, TAXES

This year, taxes will get extra tricky, because filers will be required to account for their health insurance on their forms. There are four ways to do so:

1) For taxpayers who do not have Obamacare, the process is simple: check a box indicating you have insurance. This is U.S. Individual Income Tax Return for 2014, line 61

2) If a person opted not to have any insurance, he or she needs to pay the fine/tax, which has been named the “shared responsibility payment”. This is on U.S. Individual Income Tax Return for 2014, Form 1040, line 61; Form 1040A, line 38; or Form 1040EZ, line 11. The instructions to calculate that are here, on page 5.

3) If you have a Marketplace-granted coverage exemption or you are claiming a coverage exemption on your return, fill out form 8965, and mark it on the U.S. Individual Income Tax Return for 2014, Form 1040, line 62.

4) For those who enrolled in an Obamacare plan through the Marketplace, they will have a more comprehensive section and required forms. Here’s the crucial information you need to know about the Form 1095 (Health Insurance Marketplace Statement) and the Form 8962 (Premium Tax Credit, or PTC).

The 1095a

First — please note, you must have the 1095a form to file your Premium Tax Credit form. If you are filing the Premium Tax Credit form, you can’t file a 1040 EZ form and will need to file a traditional 1040.

Now, the 1095a is a form that will be mailed to each household who enrolled in an Obamacare health insurance exchanges plan, whether it was for your state or it was a federal marketplace. The IRS is very clear: This is your proof of insurance.

The 1095a forms were supposed have arrived by January 31, the same date as W-2s and 1099s, but now it seems the new date is Feb. 2nd. You should also be able to download the 1095a form for your household from the exchange website.

The 8962

“Unfortunately, the Obamacare tax form you’ll get from your health-insurance provider won’t have all of the information you’ll need to report to the IRS. The Premium Tax Credit Form (8962), requires you to refer to your adjusted gross income on your tax return, as well as looking up the appropriate federal poverty line figure for your state. In addition, you’ll need to do many of the calculations to compare the information you provide from Form 1095a with other tax information from elsewhere on your return.”

Why do I need a form for a form?

When you applied for Obamacare coverage, you estimated your earnings for 2014. The exchange used that figure to calculate your Obamacare credit/subsidy. But, things change with income and households. Therefore, the 8962 is a worksheet to calculate the income amount again based on what you actually made in 2014; and if the figures do not match, your credit amount will have to be adjusted.

In order to be extraordinarily helpful to taxpayers wrestling with how to properly file their taxes and include their health insurance information, the IRS has published a 21 page primer. You can view the 21 pages of instructions here. This has links to three long forms and nine tip sheets.

Good luck, everyone!

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

Obama has consistently talked about how he is for “tax reform” all during his presidency. But clearly, he has no idea what that even means. True tax reform is a mechanism that produces a cleaner and clearer tax code. A great example of this was the 1986 IRC reform, where Reagan set the highest rate at 28% in exchange for eliminating massive amounts of tax shelters and gimmicks.

Obama’s cluelessness on the topic was evident during the State of the Union, where, instead of the simplification that Obama likes to espouse, we got a myriad of proposals that will further clutter the tax code. You can’t say you are for tax reform and then present a speech filled with the very items that true tax reform would remove, such expanded child care tax credits and new community college initiatives.

It is these very type of policies that have made the tax code so byzantine. Essentially the government uses the tax code to pick winners and losers favoring some but not others such as married vs non-married, children vs non-children, education vs non-education. This is the essence of crony capitalism, where politicians trade favors and barters to support certain initiatives or restrict others via new taxes or credits. They’re basically all gimmicks to aid in reelection or pander to a portion of the electorate — and then we never get rid of all the tacked-on programs and policies because no one wants to give up their special initiatives. The code is immensely complex because of it.

The tax code should never be used in this manner. It’s either a proper tax or not — but you don’t put an item into the tax code and then restrict it to certain people and not others. If someone is making more money, they are subjected to higher tax margins. Fine. But you don’t then add on more crony restrictions or surtaxes to try to squeeze out extra revenue. If a policy is good for the middle guy, it ought to also be good for the wealthier guy — who is already getting dinged accordingly (“paying his fair share”) by paying higher tax rates.

Obama’s version of “tax reform” is unrealistic and firmly rooted in his vision of “middle class economics”. This means using the tax code to promote “fairness” by targeting the wealthy to pay for new spending programs and credits for others. That is not tax reform — that is wealth redistribution.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

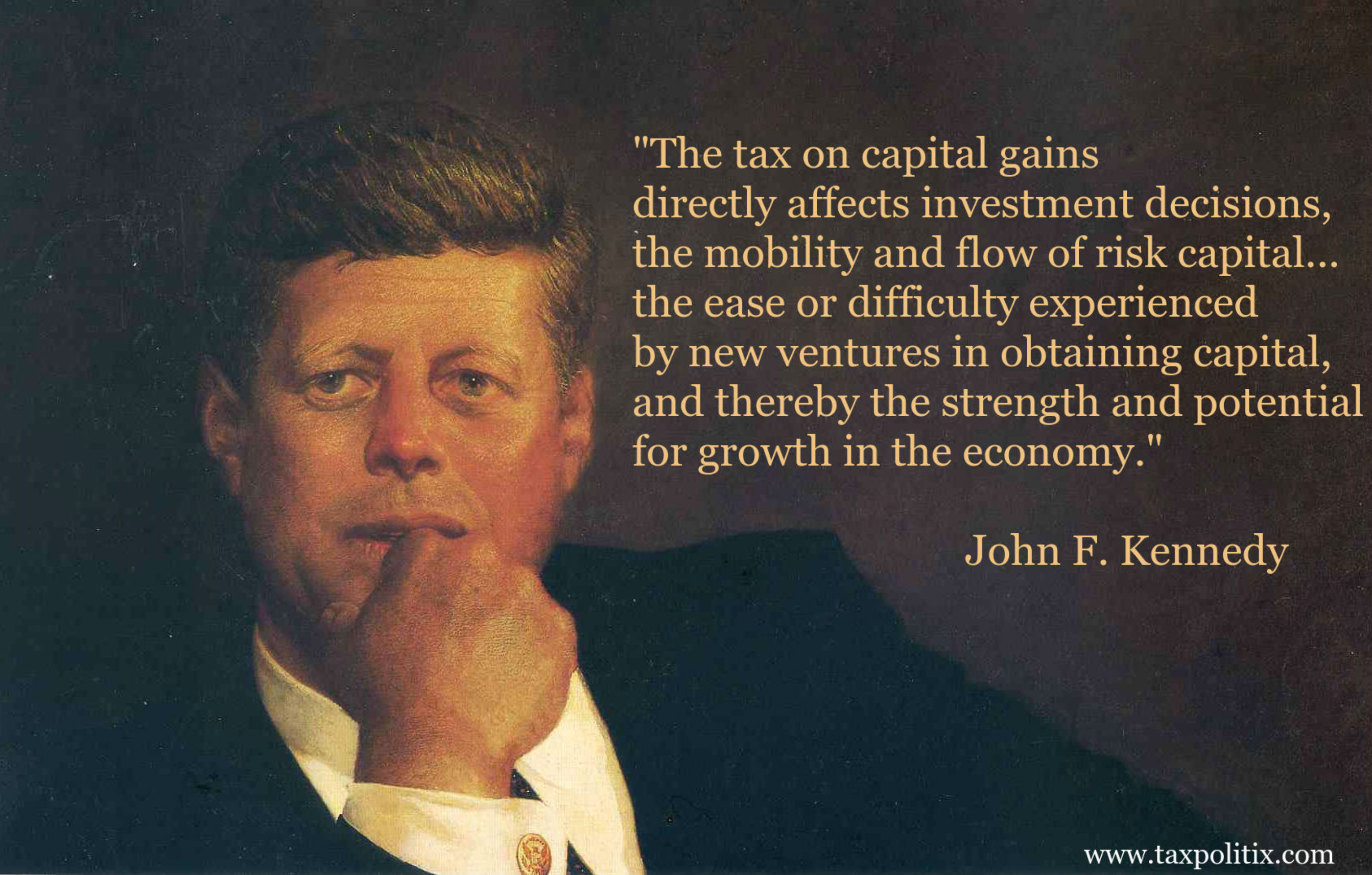

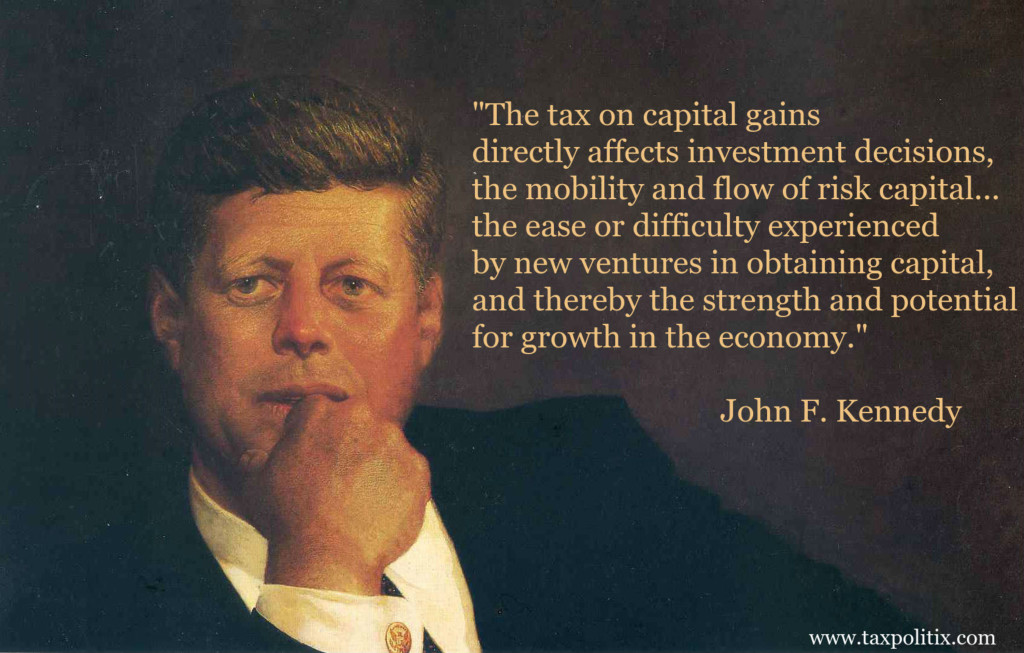

Back in 2008 when Obama was debating Hillary Clinton on national TV, Obama discussed with the moderator how raising the capital gains rate would likely reduce federal revenue collections, but he insisted it was good policy anyway — because it was a policy of “fairness”.

Why would raising the capital gains tax be a revenue loss? The effect of higher taxes slows the economy because those paying the higher capital gains have less money to invest. Unfortunately, such a policy was implemented in 2013 when capital gains went from 15-20% and was coupled with the new 3.8% surtax on investment income to pay for Obamacare, making the rate 23.8%.

Now he wants to tax, yet again, the very type of taxpayers who have money to create jobs and/or invest, by raising the capital gains rate up to 28%. This is essentially about an 18% tax hike on high income earners — two years after the last capital gains rate increase. That’s practically doubling the rate in just a few short years. And during this time, the economy has remained sluggish.

It’s a shame that Obama continues to push for policies that would have a negative effect on jobs and the economy in an effort to promote “fairness through taxation” and pay for his pet projects (such as free community college!). The concept of an American President continuing to go after people making a lot of money it is particularly loathsome; it also displays an absolute lack of familiarity with and respect for how people get wealthy — he just wants their hard-earned money.

Back in 2008 during that same debate, Obama claimed, “What I want is not oppressive taxation. I want businesses to thrive, and I want people to be rewarded for their success. But what I also want to make sure is that our tax system is fair and that we are able to finance health care for Americans who currently don’t have it and that we’re able to invest in our infrastructure and invest in our schools. And you can’t do that for free.”

But with Obama, you can do it by wealth transfer.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

The question of raising the minimum wage keeps getting pushed at the federal level, as well as across many states. If we are to educate the populace on the pitfalls of arbitrary “minimum wage” hikes, we must be sure to argue the inherent flaws of suggestion that minimum wage hikes help some people and therefore are good for everyone.

This was illustrated recently on an episode of CNBC’s “On the Money” with Becky Quick. On one side was Dan Mitchell of CATO, who has done admirable work on fiscal policy and economics over there for many years. Opposite him was Jared Bernstein, a former Chief Economist and Economic Adviser to Vice President Joseph Biden. Mitchell’s appearance on the show, however, was a bit of a disappointment on the issue of minimum wage.

There were two major points he seemed to miss. The first was in regard to the effect of a minimum wage hike on workers. Mitchell pointed out, correctly, that 500,000 people would lose their jobs, to which his opponent, Jared Bernstein, countered that 24 million people would gain more money (“get out of poverty” per the CBO), and therefore, quantitatively, people would benefit in a 50-1 ratio. But that is wrong!

Those 24 million, though they may benefit from a raise, will really one see a few cents more an hour. Those that lose their jobs, will lose not only $7.50 an hour in comparison, but also the opportunity to learn working skills and actually have a job from which they can advance in the workforce. Even if Bernstein’s figures were perfectly accurate – which they were not – having 24 million people earn a few more cents per hour versus the entire loss of jobs and livelihood do not make raising the minimum wage worthwhile.

But that point is secondary. The primary issue – and the one that Mitchell (as well as all of us who understand the economics of minimum wage) seem to be unable counter to the Jared Bernsteins of the world – relates to the economic cost of a minimum wage. He needed to explain to Mr. Bernstein that the apparent extra money going to those getting the higher minimum wage is, in fact, detrimental to the economy as a whole, and therefore ultimately to even those people it was intended to help.

Economics 1a would explain (looking for “what is unseen” ) that the extra money going to those benefiting must be coming from somewhere (though providing no extra result). It is coming from either a) lower wages paid to other employees, b) lower profits to the business, which lowers rate of return directly reducing new investments in that business and reducing the likelihood that new businesses will be started, or c) higher prices to the consumer, which (Economics 1a again) shows will reduce total sales volume, and therefore GDP as a whole..

Though Mitchell did successfully argue the merits of how minimum wages certainly shouldn’t be a federal law, but rather a state consideration, he missed entirely the ability to counter the false argument concerning the minimum wage altogether. If we don’t oppose and expose the core flaws, we will certainly continue to lose in the public square on the issue of minimum wage.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, HYPOCRISY, OBAMA, POLITICS, TAXES

President Obama ended the State of the Union address in a new way. He didn’t say, as tradition, “God bless you, and God bless these United States of America”

He said, “Thank you, God bless you, and God bless this country we love.”

A quick check on his prior SOTU speeches reveals he used the customary phrasing in past years:

2014: God bless you, and God bless the United States of America.

2013: “Thank you. God bless you, and God bless these United States of America”

2012: “Thank you. God bless you, and God bless these United States of America”

2011: ” Thank you. God bless you, and may God bless the United States of America. ”

2010: “Thank you. God bless you. And God bless the United States of America.”

What happened to “God bless the United States of America”?

Update #1: It is fairly standard for the President to end his speech this way, at least in modern times. Curious as to the reason for the shift. Here’s a little background comparison:

“Presidents from Roosevelt to Carter did sometimes conclude their addresses by seeking God’s blessing, often using language such as ‘May God give us wisdom’ or ‘With God’s help.’ But they didn’t make a habit of it. In fact, five of the eight presidents during this period concluded this way in less than 30% of their speeches. Harry Truman, Lyndon Johnson and Ford did so a bit more often, but still none of these presidents concluded even half of his addresses this way. Reagan, on the other hand, ended 90% of his major addresses by requesting divine guidance. George H.W. Bush also did so in 90% of his speeches, and Bill Clinton and George W. Bush followed suit 89% and 84% of the time, respectively.”

Update #2: Apparently, Joni Ernst said roughly the same thing. “”May God bless this great country of ours, the brave Americans serving in uniform on our behalf, and you, the hardworking men and women who make the United States of America the greatest nation the world has ever known.”

Was it a mirror to Obama’s ending? The custom, obviously, is not expected by others as it is by the President, which is why it was noticeable when Obama ended his speech. Thoughts?

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

If you plan to tune in tonight to the State of the Union, I’ll be running an Open Thread over at Bearing Drift, Virginia’s premier conservative media group. Join me over there at 8:45 to discuss Obama’s proposals.

The main theme of the evening is “middle class economics”. These include:

–raising “$320 billion over the next 10 years in new taxes targeting wealthy individuals and big financial institutions to pay for new programs designed to help lower- and middle-income families”.

–raising the capital gains and dividend tax rates to 28% on some higher earners

–creating a “fee on the liabilities of about 100 big financial institutions”

–tax credits to small businesses to help “cover costs” of requiring “employers without 401(k) plans to make it easier for full-time and part-time workers to save in individual retirement accounts”

–expanding tax credits for child child care

—expanding paid sick leave and “to fund Labor Department feasibility studies on paid leave”

—providing two years free of community college tuition for up to 9 million students

You can join in tonight as I comment and engage with other like-minded folks. See you there!

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, SOCIAL SECURITY, TAXES

Last week, the Washington Examiner did a nice job covering the growing Social Security Disability Insurance (SSDI) crisis, and Congress’s recent response to it. The issue at stake is the 2016 benefit adjustment, which would cut 20% of benefits for more than 10 million SSDI recipients:

“Many Democrats want to sweep the problem under the rug with an accounting gimmick that would merge the disability trust fund with the general Social Security trust fund, which, on paper, isn’t expected to be depleted until 2034. But House Republicans passed a rule [Tuesday] to protect the broader Social Security program from being raided.

In 1994, the payroll tax rate was reallocated between Social Security’s two trust funds to avoid depletion of the disability insurance fund, but another reallocation would ignore Social Security’s long-term funding issues.”

The idea for reallocation came from the bleak 2014 Social Security Trustees report, which described, “Lawmakers may consider responding to the impending [Disability Insurance] Trust Fund reserve depletion, as they did in 1994, solely by reallocating the payroll tax rate between [Old-Age and Survivors Insurance] and DI. Such a response might serve to delay DI reforms and much needed financial corrections for OASDI as a whole. However, enactment of a more permanent solution could include a tax reallocation in the short run.”

The reallocation response would be merely a bandaid, ignoring the overall Social Security funding crisis, which is why the House passed a rule prohibiting reallocation unless it is combined with “benefit cuts or tax increases that improve the solvency of the combined trust funds”. That is to say, there must be some act of long-term reform.

Apparently, the Left was having none of that; responses were swift and sharp. The LA Times headline screamed, “On Day One, the new Congress launches an attack on Social Security”. The paper further described how,

“The rule hampers an otherwise routine reallocation of Social Security payroll tax income from the old-age program to the disability program. Such a reallocation, in either direction, has taken place 11 times since 1968, according to Kathy Ruffing of the Center on Budget and Policy Priorities.

But it’s especially urgent now, because the disability program’s trust fund is expected to run dry as early as next year. At that point, disability benefits for 11 million beneficiaries would have to be cut 20%. Reallocating the income, however, would keep both the old-age and disability programs solvent until at least 2033, giving Congress plenty of time to assess the programs’ needs and work out a long-term fix.”

Clearly, Democrats doesn’t see the irony of having to reallocate 11 times already as an major fiscal problem. I’m betting that every time there was a reallocation, it was to give Congress “plenty of time to assess the programs’ needs and work out a long-term fix.” In other words, kick the can again because the issue is politically unpalatable.

The Washington Examiner spoke to Charles Blahous, a Trustee of the Social Security and Medicare Trust Funds, about the Social Security situation. Blahous described how “the problem is not that disability needs a bigger share of the overall payroll tax than it now has, but that Social Security as a whole faces a financing imbalance that needs to be corrected. The single most irresponsible response to the pending [disability insurance] trust fund depletion would be to do nothing other than paper it over with a reallocation of funds, delaying meaningful corrective action as long as possible.”

You can be sure the Dems will use this issue as a way to stir up the base between now and 2016. Kudos to the new Congress for being willing to discuss and tackle the insolvency problem instead of moving funds around automatically.

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, HYPOCRISY, OBAMA, POLITICS, RETIREMENT, SOCIAL SECURITY, TAXES

As a CPA, it is frustrating to hear Social Security repeatedly being described as a pay-as-you-go (“PAYGO”) system, which gives credence to something that is terribly incorrect. PAYGO is not a system at all; rather it is a method of reporting that hides earned realities, making it totally unacceptable to accounting professions, the SEC, and virtually everybody outside the government.

The fallacy of calling it PAYGO is that, in reality, the cash includes everything we are getting in, while the cash out doesn’t include the responsibilities due to come. The cash out formula specifically excludes the trillions promised to existing workers in the future, (while their Social Security tax is being collected today). It doesn’t really describe, as part of the expenses being incurred this year, the amount of future retirement benefits being earned and promised.

In contrast, if you give an insurance company today $100,000 to pay you a retirement pension beginning when you retired at the age of 65, the insurance company (logically and legally), the insurance company would report this as an asset offset by a liability to provide $100,000 of payments in the future. The Social Security system, however, reports that as $100,000 of profits in the year received, while the obligation to account for and provide future benefits is incredibly ignored.

When the cash in is received, that money egregiously goes into the government’s general tax revenue account and not in any Social Security Fund (anymore). The Social Security Administration merely collects and records the gross Social Security tax receipts, while the net amount, after deductions, is sent to the IRS. Yet the gross amount recorded is the amount spent by the government, resulting in the staggering deficit we face today. Therefore, it is outrageous for anyone to say that accounting for the system can be done simply by looking at the cash in-cash out.

The biggest problem with this arrangement is that it puts the burden on the wrong people. We have a growing population of retiring taxpayers and the current generation is paying off the obligation the older generation never paid for. It is a Ponzi scheme in which, depending on how you play it, you manipulate who is paying whose obligation. Therefore, the PAYGO method doesn’t work because the government takes 100% of the money they receive and they do not put away; they need it to pay today’s debt to another taxpayer, while today’s payee is stuck holding the bag.

For several years now, the Social Security trustees reports have noted Social Securities unfunded liabilities – those promises made to individuals solely in exchange for amounts they have already paid for – to be trillions in deficit. Social Security in its present form is unsustainable.

The term PAYGO is used for the lay person; cute semantics – but misleading at best, willfully dishonest at worst. It mischaracterizes the program for the political purpose of allowing politicians to declare that Social Security does not contribute to the deficit, and therefore, should not be overhauled in any major way. But until we agree to start recording Social Security (and Medicare) in budgets in actuarially sound way, we will never be able to honestly and effectively deal with their fiscal crises.

How we talk about and understand Social Security and its funds needs acute attention because we face another looming crisis of funding: Social Security’s Disability Insurance (SSDI). SSDI benefits are slated to be cut by 20 percent near the end of 2016, at the same time that SSDI has seen a massive increase of recipients in the last few years. This is certain to be a major issue for the Presidential elections.

Already the Democrats are stirring up the base on this issue. Last week, Sen. Elizabeth Warren claimed that “The GOP is inventing a Social Security crisis that will threaten benefits for millions & put our most vulnerable at risk”. Obviously this is patently false. The entire Social Security program needs massive reform instead of incrementally kicking the can further down the road to avoid making difficult, but necessary changes for the long haul.